The Money Milestones in your 30s

By the time you reach your 30s, you should have already gotten a head start toward saving for retirement and for your children’s future. However, life does not always happen as planned. When children enter the picture, our employment situation changes, or we are hit with unexpected medical bills.

An individual investor today is very fortunate. The amount of information available is absolutely mind-boggling! There are multiple sites on the internet to identify the right investment vehicle. Be it PPF, Sukanya Samriddhi Scheme, Debt Mutual Funds, Equity Mutual Funds, SGB or digital gold – today investor is spoilt for choices and information.

This makes it quite challenging to find the right way to go about planning your finances. In this article, I list 4 steps 30-year-olds can take to better their future.

Determine what your ideal retirement looks like

The cardinal rule of investing is never to put all your eggs in the same basket. Different asset classes move differently at any given period. You should have a balanced portfolio to minimize risk. But, doing this is quite complex.

It is ideal to have assets in various accounts. The assets themselves are of different kinds – stocks, bonds, cash, Mutual Funds, ETFs, etc. Once that is done, the ideal asset allocation must be determined. Current asset allocation must be calculated and compared to see the skew. This could easily take an entire weekend!

The first step any couple or individual in their 30s needs to take is determining what their ideal retirement looks like. Would you like to live in a wealthy community, travel a bit, and even help your children and grandchildren out? Make sure you plan accordingly.

It is no secret that you cannot rely on your PF to support you through a comfortable retirement. In fact, any EPF/NPS benefits will only serve as padding to a well-planned retirement fund that has grown over the years.

Most bonds and debt investment vehicles cannot keep pace with inflation. They can only be considered to preserve the capital at best. Hence there is a need to keep equity Mutual Funds as a core part of the investment portfolio. Among equity Mutual Funds, there are different categories including large-cap, mid-cap, small-cap funds.

The earlier you begin saving for this the lesser you will need to save. It may seem too good to be true. Even Albert Einstein allegedly called compounding “the greatest mathematical discovery of all time.” There is no sleight of hand involved, but—as with most “magic”—what is really going on is a lot simpler than you might think.

If you can start saving and investing your money regularly from a young age, and continue to do it sensibly, the amount of wealth you will have after 25-30 years will be huge and more than enough to meet your financial goals (like your retirement, or a child’s education and marriage).

In fact, our calculations show that if you can save just Rs. 1,500 per month and let this money compound at an estimated 12% return every year for 25 years, you will end up with around Rs. 28 lac at the end of this 25-year period!

If your money can earn an estimated 15% return per annum instead of 12%, your monthly investment of Rs 1,500 that you make for 25 years, would grow to a huge Rs 48 lac! approximately.

Mutual Fund companies such as L&T Mutual Fund also have hybrid funds with a fixed allocation of equities and debt components. Such hybrid funds are ideal for reducing the risk associated with pure equity investments.

Using a SIP calculator, an ideal amount can be invested through a Systematic Investment Plan. This will cut down on unnecessary costs, create a sound investment plan, and get the most out of your paycheck and benefits.

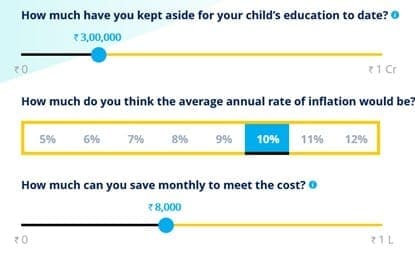

Start a college fund for your kids

For children, typical goals will be:

- School admission at 4

- Miscellaneous large expenses every few years (school trips etc.)

- College at 17-18 (4 years + 1 year of preparation time: so, 5 goals in total: Admission1, Year1, Year2, Year3, Year4: I have made this one goal in the example, but you should ideally make it as 5)

- Postgraduate (2-3 years, timing unknown, > 23y)

- Marriage (timing unknown)

One way to maximize your educational savings is to invest in Equity Mutual Fund. You can calculate how much your child may require using this calculator which is designed to help people put away money for college.

For each goal you can follow this standard goal-setting approach:

- Find horizon of goal, cost of goal today, inflation.

- Create a portfolio per goal with an asset allocation suitable for the horizon: Equity Mutual Fund, long term debt (like PPF), short term debt (money market, liquid fund)

- Setup SIPs and rebalances every year.

Time and money are great friends:

If you can leave your money to spend a long time with time, they can work wonders for your wealth. Just start investing as early as possible instead of waiting till you grow older and have less time to compound your money. Even a 10-year delay can cause problems for you.

Marginally higher rate of return creates a huge difference:

As you just read above, Rs 1,500 per month invested at 12% for 25 years will leave you with around Rs. 28 lac. Just a 3% higher return, i.e., 15% for 25 years will leave you with a much higher around Rs. 48 lac!

That is why, if you want to invest your money for the long run, say 15-20 years, invest it in assets that have the probability of giving the highest long-term returns.

Pay off your debt!

This is a no-brainer: The more you owe, the more your debt will grow in the long run. If you have a mountain of debt that makes you anxious just thinking about it, do not fret. Make a list of everything you owe, from credit card debt and lingering student loans to car payments and mortgage payments. Focus on staying on top of your monthly payments and each month’s added interest to prevent these from snowballing.

If you are not sure where to start, tackle high-interest debt first to save that money for the future. Ideally, your 30s offer slightly more financial flexibility than your 20s, allowing you to simultaneously tackle debt and save for retirement in order to keep your finances in good standing both now and in the future.

Keep an emergency fund handy!

It may seem daunting to build up an emergency fund, but you can do it by adding a little bit to the fund every month until you feel that you have enough money to comfortably get you through an emergency, whether it is a complicated medical situation or a job loss. With an emergency fund, you will have more financial flexibility to battle through the dry season.

Experts suggest that you should have between three- and six-months worth of minimum monthly expenses saved up for just-in-cases. And if that emergency does arise, do not spend more than you have to, and focus on getting back on your feet as soon as possible by being proactive.

Laid off? Go find that dream job and show them what you are capable of—it is never too late to start saving for the future money milestones.

Most importantly!

Do not forget to invest in yourself through on-job training/advancement, formal and continuing education. Make yourself valuable to the workforce so when you ask for that raise you will get it. And if you do not, take your skills elsewhere to command the money milestones your skills deserve.

Always have the habit of reading the scheme-related documents before investing to understand the scheme type, investment patterns, and the risk factors associated with particular investments, and consult your financial advisor to understand the implication of any investment.

Disclaimer: This information is for general information only and does not have regard to the particular needs of any specific person who may receive this information. L&T Investment Management Limited, the asset management company of L&T Mutual Fund or any of its associates; does not guarantee/indicate any returns/and shall not be held liable for any loss, expenses, charges incurred by the recipient. The recipient should consult their legal, tax, and financial advisors before investing. The recipient of this information should understand that statements made herein regarding future prospects may not be realized or achieved.

Mutual Fund investments are subject to market risks, read all scheme-related documents carefully.